What's Difference Between Standing Order And Direct Debit

Hey there, money maestros and everyday spenders! Let's have a little chat about something that might sound a bit… well, boring. But trust me, understanding the difference between a Standing Order and a Direct Debit can actually be a real lifesaver for your wallet and your peace of mind. Think of it as knowing the secret handshake to your bank account!

We all have bills to pay, don't we? Rent, mortgage, that Netflix subscription that's practically a family member now, maybe even a little treat for yourself every month. And getting those payments sorted smoothly means less stress and more money for fun stuff. So, let's dive into these two handy payment methods and see what makes them tick.

Standing Order: Your Reliable Buddy

Imagine you've got a friend, let's call her Penelope. Penelope is super organised and always remembers your birthday. Every month, on the 15th, she automatically sends you a little gift. She doesn't need to check with you if you're okay with it, or if the amount is right, she just does it because that's the arrangement you set up.

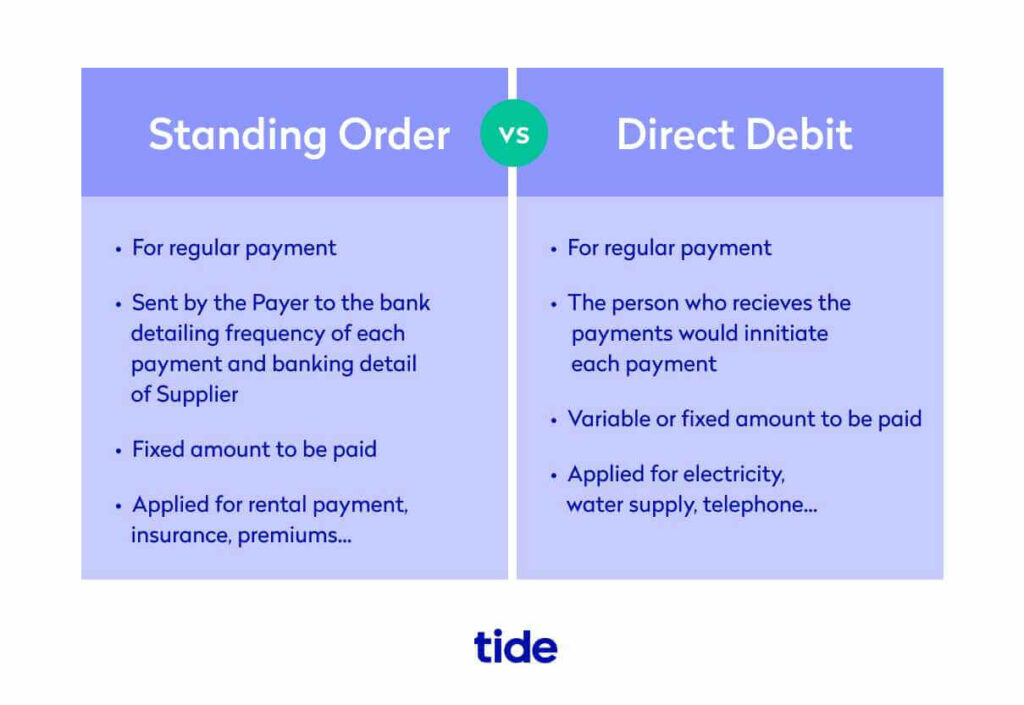

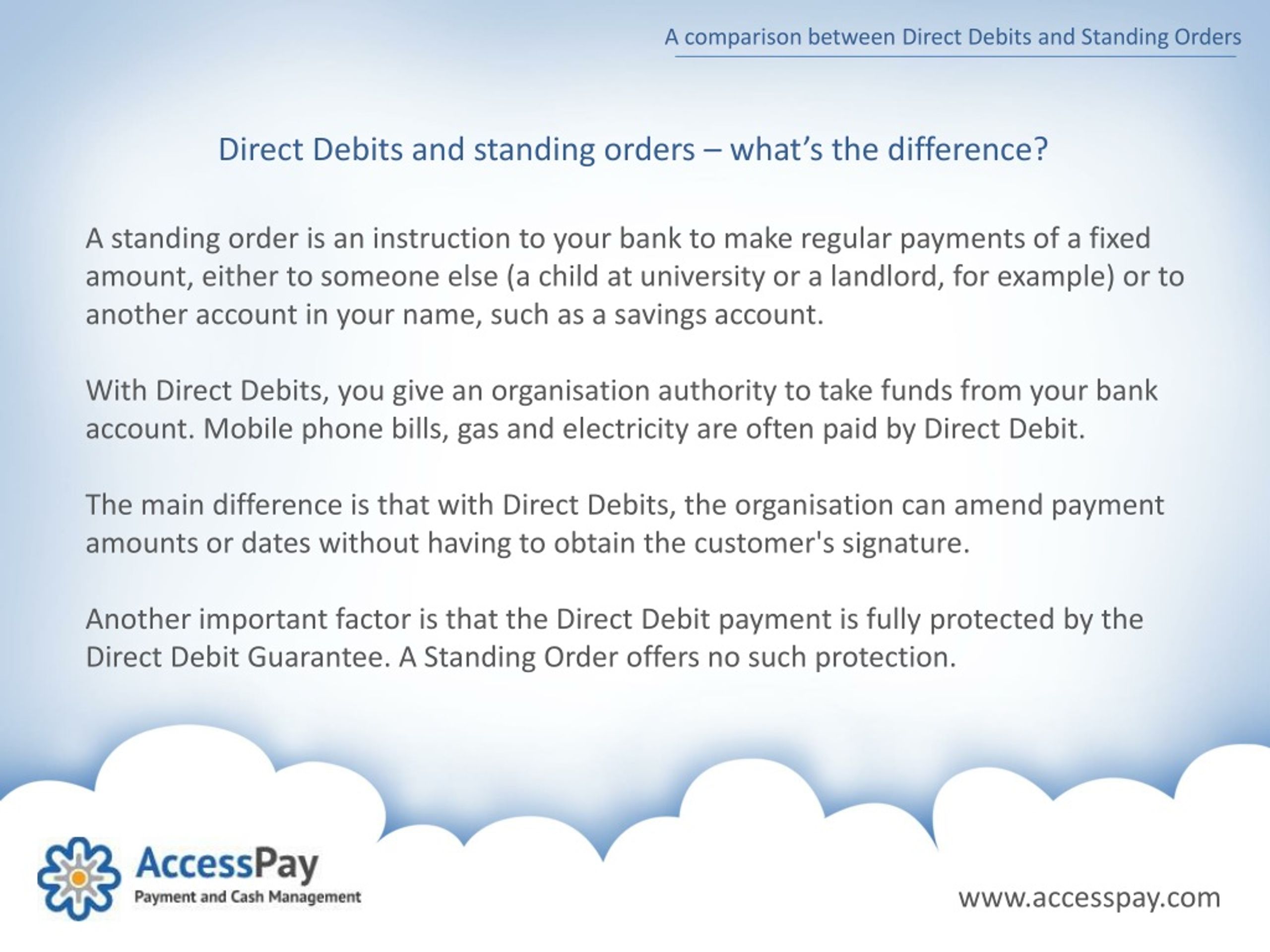

A Standing Order is pretty much exactly like Penelope. You tell your bank, "Hey, please send £X to Y person or company on Z date, every month." And your bank, being the good little soldier it is, just does it. It's a fixed amount, on a fixed date, and it’s always the same. Think of it as setting a regular allowance for yourself, or sending pocket money to your kids.

This is brilliant for things like:

- Rent or mortgage payments (if they're the same amount each month).

- Regular savings contributions to your emergency fund or that dream holiday pot.

- Money you send to family members consistently.

- Charity donations that you want to make without thinking.

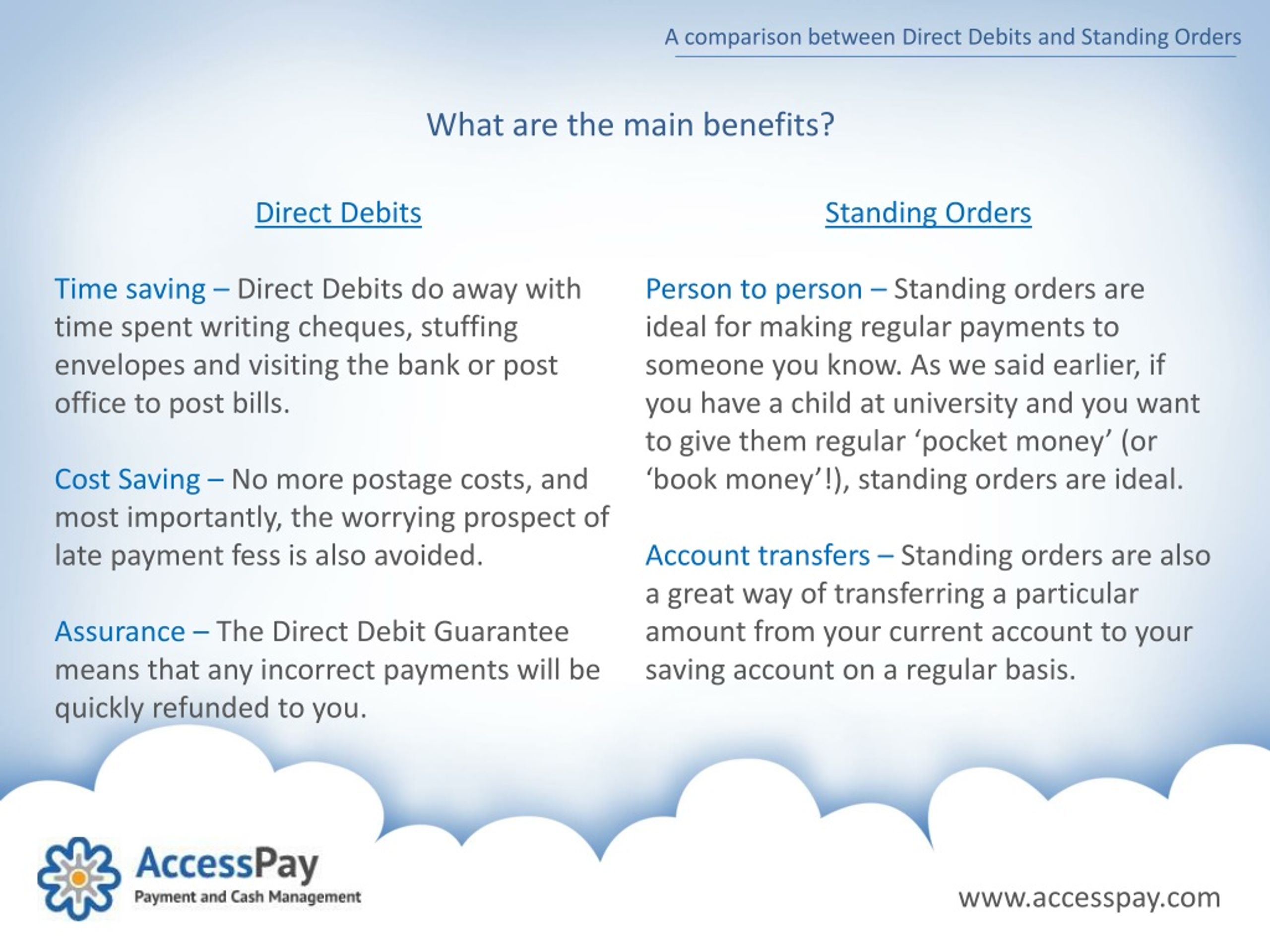

The big upside here is that you are completely in control. You set it up, you can change it, and you can cancel it whenever you like. It's like having a personal butler for your regular payments, but it only does what you tell it to do, precisely and on time.

For instance, my aunt Carol absolutely adores her Standing Order for her beloved cat, Mittens. Every month, on the 1st, £50 whizzes from her account to the vet's practice for Mittens' ongoing health plan. She set it up years ago, and it’s just there, a quiet, reliable part of her finances, ensuring Mittens always has access to the best feline care. She doesn't have to remember, she doesn't have to do anything, and Mittens is very grateful!

It's the "set it and forget it" option, but with a healthy dose of your direct command. You're the boss, and the bank is just following your orders. Simple, right?

Direct Debit: The Flexible Friend

Now, let's meet Reginald. Reginald is a bit more… dynamic. He's the friend who always brings a surprise to the party, or who might pay for everyone's pizza one night and then send you a message asking for their share the next. Reginald's payments can vary, and he might need to check in with you about the exact amount.

A Direct Debit is a bit like Reginald. It's an arrangement you make with a company, not just your bank. You give them permission to take money from your account, but you can also set limits and you’ll usually get advance notice of any changes. This is super useful when the amount you owe can change each month.

Think about things like:

- Your electricity or gas bill – it’s definitely not the same amount every month, is it?

- Your mobile phone contract – sometimes you might go over your data allowance and the bill goes up.

- Gym memberships or magazine subscriptions.

- Credit card payments.

The company you owe money to tells your bank how much they need to take, and when. But here's the crucial bit: you are protected by the Direct Debit Guarantee. This is a big deal!

The Direct Debit Guarantee means:

- You'll get advance notice of any changes in the amount or date of payment.

- If an error is made, you'll get an immediate refund.

- You can cancel a Direct Debit at any time by contacting your bank.

So, while it seems like the company has more control, you actually have a lot of safeguards in place. It’s like having Reginald as a friend, but knowing he’ll always give you a heads-up before he asks for money, and if he messes up, he’ll sort it out straight away.

My neighbour, Brenda, uses Direct Debits for everything that varies. Her broadband bill, her council tax (which changes annually), and even her online grocery shop. She loves it because she doesn't have to log in to multiple websites and remember to pay each one. The money just comes out, and she gets an email beforehand. If she sees a charge that looks a bit off, she just calls her bank, and usually, that’s that. It's her way of outsourcing the monthly bill-juggling act.

Why Should You Care? (Besides Avoiding Late Fees!)

Okay, so Penelope and Reginald are fun analogies, but why is this actually important for your everyday life? Well, it boils down to a few key things:

1. Avoiding Late Fees and Hassles

This is the most obvious one. Missing a payment can mean hefty late fees, interest charges, and even a black mark on your credit history. Imagine forgetting to pay your car insurance and then having to pay a massive premium because you're seen as a higher risk. Ouch!

Both Standing Orders and Direct Debits help you avoid this by automating payments. It's like having an automatic reminder system built into your bank account. Your bills get paid on time, keeping your financial life smooth and your providers happy.

2. Budgeting Made Easier

When you know exactly what fixed payments are going out each month via Standing Order, it’s much easier to create a realistic budget. You can see your predictable outgoings and then allocate the rest of your money for groceries, fun, and savings. It gives you a clear picture of your financial landscape.

Direct Debits, while variable, can also help with budgeting because you get advance notice. You can see if your energy bill is going to be higher than usual and adjust other spending accordingly. It’s like getting a heads-up from your bank about upcoming financial weather.

3. Convenience and Peace of Mind

Let's be honest, in our busy lives, who has time to remember every single payment deadline? Setting up automated payments frees up your mental energy and reduces the stress associated with managing finances. It’s one less thing to worry about.

You can go on holiday, have a hectic work week, or just be a bit forgetful, and your essential payments will still be made. That's pretty darn sweet, wouldn't you agree?

4. Protecting Your Money

The Direct Debit Guarantee is a fantastic safety net. If a company takes the wrong amount or tries to take money without permission, you have the right to a refund. This isn't something you automatically get with other payment methods. It gives you an extra layer of security when dealing with companies whose payment amounts can fluctuate.

The Bottom Line

So, to sum it up:

A Standing Order is your personal, fixed-amount, fixed-date instruction to your bank. It’s like Penelope, your reliable, predictable friend.

A Direct Debit is an authorisation you give to a company to collect payments from your account, often with variable amounts, but with your protection and advance notice. It’s like Reginald, your dynamic friend who keeps you in the loop.

Understanding which one is best for which situation can save you money, stress, and a whole lot of potential headaches. It’s not about being a financial wizard; it's just about knowing how to use the tools your bank provides to make your life a little bit easier and a lot more organised. So next time you’re setting up a payment, ask yourself: am I Penelope or Reginald? And enjoy the smooth sailing that comes with it!